Click to see the full-size image

While Washington remains focused on geopolitical flashpoints in Europe, Middle East and the South China Sea, a quieter yet strategically consequential transformation is unfolding along the western shores of the Indian Ocean. In this evolving landscape, East Africa – particularly Kenya, Tanzania, and Mozambique – is consolidating its position as a critical interface between global trade routes, resource flows, and regional integration dynamics.

With a combined population approaching 150 million and economic growth rates consistently exceeding the global average, the region can no longer be treated as peripheral to global economic strategy. Instead, it is emerging as a contested space where infrastructure development, supply chain integration, and geopolitical influence intersect in increasingly complex ways.

This shift is not occurring in isolation. It reflects broader structural changes in the global economy, including the growing importance of critical minerals and the search for alternative logistics corridors amid persistent disruptions in traditional trade routes. Against this backdrop, East Africa’s geographic position and resource endowment have acquired renewed strategic significance.

The central question, therefore, is no longer whether the region matters, but which external actors are shaping its integration into the global economy – and on whose terms.

The map of Swahili Coast

The Northern Corridor

At the center of East Africa’s economic transformation lies the Port of Mombasa, which functions not merely as Kenya’s principal maritime gateway but as a critical access point for the entire continent. Through the 1,700-kilometer Northern Corridor, the port connects landlocked economies – including Uganda, Rwanda, Burundi, and the eastern regions of the Democratic Republic of Congo – to global markets. It serves both as a logistical backbone and a mechanism of regional economic integration.

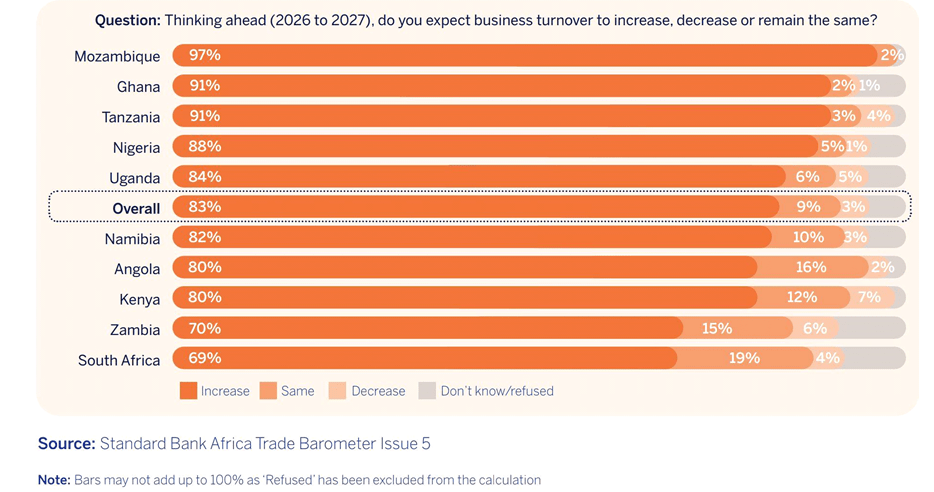

Recent data underscores the structural nature of this transformation. According to the Standard Bank Africa Trade Barometer, East Africa recorded a 10-percentage-point increase in export activity, driven by a combination of infrastructure investment and policy coordination.

Regional governments have stepped up their efforts to reduce long-standing frictions in intra-African trade. Kenya and Tanzania have renewed their commitment to dismantling the non-tariff barriers that have historically increased transaction costs and delayed cross-border flows. At the institutional level, corridor authorities have started to coordinate more closely and have signed agreements aimed at addressing freight costs, which remain significantly above global benchmarks.

The port of Mombasa, Kenya

The result is not simply improved efficiency at individual nodes, but the incremental consolidation of a more coherent regional trade system. Infrastructure upgrades across ports, railways, roads, and digital customs platforms are beginning to function as interconnected components rather than isolated investments.

This distinction is critical. Without efficient inland connectivity, a port remains a bottleneck, while regulatory harmonization without physical infrastructure yields limited practical gains. In East Africa, these elements are being developed together more and more, reinforcing each other and enabling an integrated economic space.

What is emerging is not just a series of national infrastructure projects, but the early stages of a regional market encompassing more than 300 million consumers. As connectivity improves and trade barriers decline, the Northern Corridor is evolving from a transport route into a structural foundation for long-term economic integration.

The survey by Standard Bank Group (South Africa)

What the Trade Data Reveals

The Standard Bank Africa Trade Barometer, which tracks business sentiment across major African markets, indicates consistent improvements in infrastructure quality, trade openness, and access to finance across a majority of East African economies.

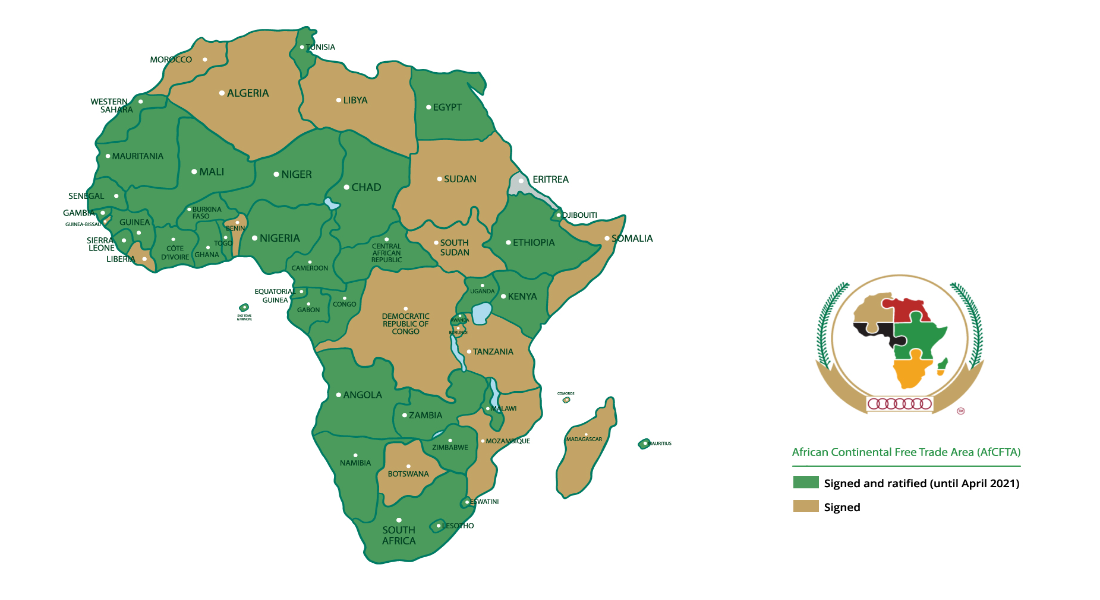

Awareness of the African Continental Free Trade Area (AfCFTA) is expanding, and early implementation efforts are beginning to translate into measurable trade flows. At the same time, moderating inflation and improved external debt conditions in several economies provide a more stable macroeconomic environment for growth.

Within this broader continental context, East Africa stands out as a leading subregion. The observed increase in export activity reflects not only favorable commodity conditions, but also tangible improvements in trade facilitation. Corridor development, customs digitization, and regulatory coordination are reducing the friction that has historically constrained intra-African trade.

One of the most significant developments is the gradual shift from competitive to complementary port dynamics. Coordination between major gateways – such as Mombasa and Dar es Salaam – suggests a move toward network-based logistics rather than zero-sum competition. This, in turn, enhances the efficiency and resilience of regional trade systems.

The implication is that trade growth in East Africa is becoming increasingly system-driven, rather than dependent on isolated policy changes or external shocks.

African Continental Free Trade Area (AfCFTA)

The Battle for Advantage: China and System-Level Integration

External engagement has played a decisive role in shaping this transformation, with China emerging as the most systemically influential actor. Western assessments of Chinese involvement in African infrastructure – particularly port development – have often been framed through a security lens, emphasizing potential dual-use capabilities and long-term military implications. While such concerns are not unfounded, they capture only a narrow dimension of Beijing’s broader strategy.

In practice, China’s approach is defined less by the acquisition of individual assets and more by the construction of integrated economic systems. Across Africa, Chinese entities have participated in the development of more than 30 commercial ports in over 15 countries. These projects are rarely standalone investments. Instead, they are embedded within larger networks that include railways, highways, industrial zones, and digital infrastructure.

This integration is crucial to their strategic value. By linking ports to inland production centers and export corridors, China is not simply facilitating trade – it is shaping the architecture through which trade occurs. Technical standards, financing structures, and supply chain relationships established through these projects create long-term dependencies that extend beyond the lifespan of individual investments.

Chinese construction workers in Africa

Recent developments along the Swahili Coast illustrate this pattern. Upgrades at the Port of Mombasa continue alongside expanded logistics networks. Construction initiatives in Tanzania – including port infrastructure and associated energy facilities – are being developed in coordination with transport corridors that connect resource-rich internal regions to coastal export points. Each of these elements reinforces the others, contributing to the emergence of a more tightly integrated economic system.

This model operates across multiple layers simultaneously. Physical infrastructure is complemented by financial arrangements, technical expertise, and commercial partnerships, all of which are formed in ways that align host economies with Chinese supply chains. The cumulative effect is not immediate dominance, but gradual system-level influence.

China-funded railroad in Kenya

Critical Minerals and the Geography of Leverage

China’s position in East Africa is further reinforced by its role in structuring critical mineral supply chains, where control over processing and downstream manufacturing increasingly outweighs access to raw resources. In this context, East Africa’s mineral endowment is not simply a source of export revenue, but a strategic variable in the global competition for industrial inputs.

Tanzania’s Ngualla rare earth project illustrates the scale and significance of these dynamics. As one of the largest deposits outside China, it is expected to supply tens of thousands of tons annually over multiple decades. But the strategic importance of such projects lies less in extraction volumes than in how output is integrated into global processing networks. Without domestic refining capacity, resource-rich states remain dependent on external actors for value addition.

China’s advantage is most pronounced precisely at this stage. It controls a dominant share of global rare earth processing, separation, and magnet manufacturing capacity – segments that generate the highest value and confer the greatest strategic leverage. As a result, even where extraction occurs outside China, downstream dependency often persists.

This pattern extends beyond rare earths. Chinese companies have secured access to lithium assets across the African continent, ensuring upstream supply for electric vehicle production and battery manufacturing. At the same time, state-backed financing – often deployed through concessional or semi-commercial lending – has enabled Chinese companies to participate across multiple stages of the mineral value chain.

The implication is structural rather than transactional. By integrating extraction, processing, and manufacturing into interconnected systems, China can influence pricing, technological standards, and long-term industrial dependencies. In such a framework, control over minerals is exercised less through ownership of deposits than through dominance of the systems that transform them into usable inputs.

Ngualla Rare Earths Project, Tanzania

Financial Architecture and the Role of Multilateral Institutions

While China’s influence is most evident in physical infrastructure and industrial integration, Western involvement in East Africa is more apparent in the financial and institutional sectors. International financial institutions, especially The International Monetary Fund and World Bank, play a pivotal role in promoting macroeconomic stability and managing sovereign debt throughout the region.

In Kenya, this role has become increasingly significant in the context of rising fiscal pressures and external debt obligations. Expanded engagement by multilateral lenders has focused on restoring fiscal balance, stabilizing currency dynamics, and implementing structural reforms aimed at improving long-term economic resilience. These interventions operate at the level of macroeconomic governance rather than project-specific financing.

This shift has coincided with a gradual diversification of Kenya’s external creditor base. While Chinese financing remains central to large-scale infrastructure development – particularly in transport and energy – multilateral institutions have increased their relative share of external lending. This reflects both the concessional nature of their financing and the existence of established frameworks for debt restructuring and risk management.

This evolution does not indicate a simple displacement of one source of financing by another. It points to the emergence of a layered financial ecosystem in which different actors fulfill distinct but complementary roles. Chinese capital tends to concentrate on capital-intensive infrastructure projects, while multilateral institutions focus on macroeconomic stabilization and policy reform.

From a strategic perspective, this division of roles creates both opportunities and constraints. On the one hand, it allows recipient countries to access multiple sources of capital and expertise. On the other, it can result in fragmented economic governance, where infrastructure development and macroeconomic policy are not always fully aligned.

IMF Mission Chief for Kenya Haimanot Teferra (right) and a member of the mission (left) during the meeting with Kenyan authorities, September 25, 2025

Infrastructure Under Pressure: The EACOP Case

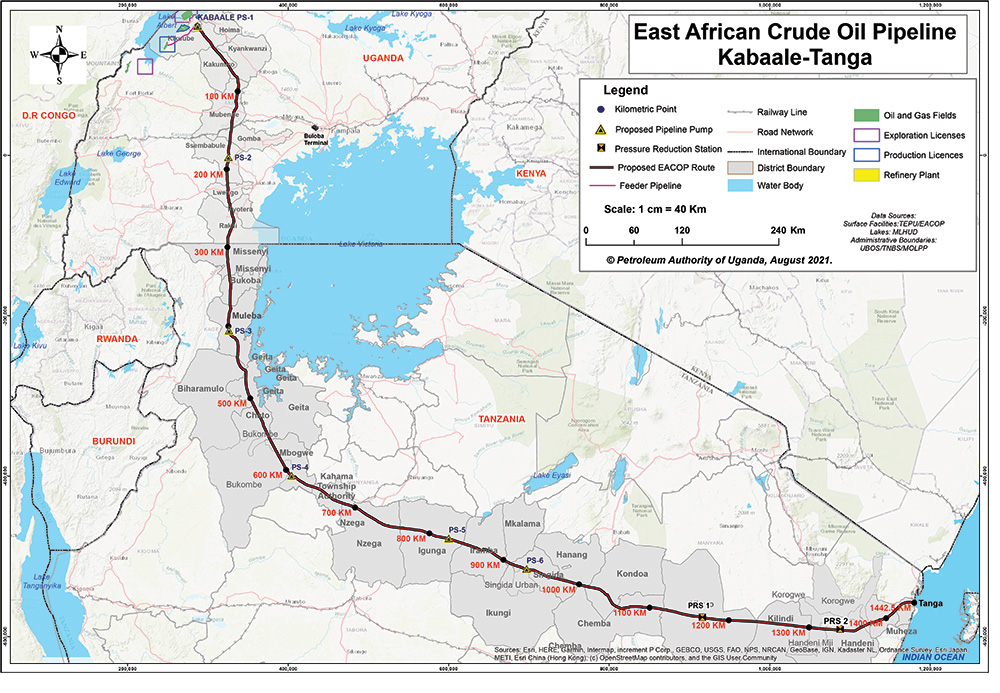

The East African Crude Oil Pipeline (EACOP) provides a particularly revealing case study of how infrastructure development in the region is shaped not only by state actors and financial institutions, but also by transnational advocacy networks.

Originally conceived as a major energy corridor linking Ugandan oilfields to Tanzania’s port of Tanga, the 1,443-kilometer pipeline was expected to be financed through a consortium of Western and non-Western financial institutions. In its initial design, the project reflected the same multi-actor financing model that characterizes many large-scale infrastructure initiatives in emerging markets.

But this model proved vulnerable to sustained external pressure. Environmental and human rights organizations launched coordinated campaigns targeting both the project and its financial backers, framing EACOP as environmentally unsustainable and socially harmful. These campaigns extended beyond public advocacy, directly engaging with Western institutional investors and shareholders of major banks.

Several Western financial institutions reassessed their involvement under the excuse of increased reputational risks. Over time, this resulted in the withdrawal of key participants, which fundamentally altered the composition of the financing structure. By the time the first major external financing tranche was finalized, the lender base had shifted toward regional and non-Western institutions, significantly slowing the realization of the EACOP project.

The outcome illustrates a broader shift in the political economy of infrastructure. Large-scale projects are no longer determined solely by host governments and financiers, but are increasingly subject to scrutiny and influence from globalist powers. These dynamics introduce new variables into infrastructure planning, including reputational risk, ESG considerations, and the potential for sustained external pressure.

As a result, the feasibility of major infrastructure initiatives now depends not only on economic viability and state support, but also on their ability to withstand transnational scrutiny.

The map of the EACOP

Negotiation, Sovereignty, and Scale: The Bagamoyo Port

The development trajectory of the Bagamoyo Port project in Tanzania highlights a different dimension of infrastructure politics: the tension between scale, sovereignty, and financing conditions.

The project was initially conceived as a $10 billion mega-port to be developed in partnership with Chinese investors. However, President John Magufuli suspended the project in 2019 after Great Britain and Japan offered a better deal. This agreement never materialized due to the absence of comparable financing packages or implementation frameworks. The scale of the required investment, combined with the project’s complexity, limited the availability of viable alternatives.

By 2025, negotiations with Chinese partners resumed, reflecting a pragmatic reassessment of available options, but the terms Beijing now offers are almost certainly less favorable than those available in 2019.

The Bagamoyo case illustrates that infrastructure negotiations are not simply economic transactions, but political processes shaped by competing priorities. Governments must weigh immediate development needs against long-term control, often in contexts where alternative sources of financing are limited.

In this sense, the project serves as a microcosm of broader regional dynamics, where engagement with external powers involves continuous recalibration rather than fixed alignment.

The Bagamoyo Port in Tanzania

The Indian Dimension: Networks Over Scale

India’s role in East Africa differs fundamentally from the approaches of both China and the West. Unlike China, India does not engage in infrastructure financing on a comparable scale. Unlike Western actors, India’s influence is not centered on institutional or macroeconomic engagement. Instead, India’s influence is rooted in its long-standing commercial and cultural networks with its African diaspora, which consists of over three million people, primarily on the Swahili coast.

These connections are not recent developments. Trade links between the Indian subcontinent, the Arabian Peninsula, and the East African coast date back centuries, facilitated by merchant communities such as the Bhatia, Bohra, Khoja, and Jain networks. Operating through maritime routes historically interconnected with Oman, these communities established enduring commercial ties long before colonial boundaries and modern state structures existed.

These legacy networks continue to shape economic interaction. Indian businesses maintain a strong presence in sectors such as trade, manufacturing, and services, often operating through family-owned enterprises with deep local integration. This embeddedness provides a form of resilience that differs from capital-intensive, project-based engagement.

India’s strategy, therefore, is less about transforming physical infrastructure and more about sustaining influence through human and commercial relationships. As global supply chains become more fragmented and geopolitical alignments more fluid, such networks may prove to be comparatively durable, precisely because they are not easily replicated or withdrawn.

Kenyan-Indian celebration

The Russian Variable: Limited Presence, Latent Capacity

Russia’s presence along the Swahili Coast is limited in economic and infrastructural terms. Moscow has not engaged in large-scale port construction or transport development, nor has it played a central role in financial governance or trade frameworks. Its current footprint is modest and primarily concentrated in the security domain.

This presence is most visible in military cooperation and training programs. Tanzania, for instance, has maintained limited but consistent engagement with Russian military institutions, including the training of personnel in Russian academies. Such activities, while not transformative in scale, establish channels of interaction that can be activated under specific conditions.

The Russian training ship Smolny docked in Dar es Salaam, Tanzania, August 16, 2025

The strategic significance of this presence lies less in its current impact than in its potential responsiveness. In other regions of Africa, Russia has demonstrated an ability to deploy relatively low-cost, modular security arrangements in response to instability or governance vacuums. These models do not require extensive infrastructure or long lead times, allowing for rapid engagement when opportunities arise.

In the context of East Africa, this creates a form of latent capacity. Under conditions of political instability, insurgency escalation, or shifts in Western security engagement, Russia could expand its role more quickly than actors constrained by more complex decision-making processes.

While Moscow is not currently a major player in the region, its strategic posture is defined by optionality rather than absence.

For external actors, East Africa represents both opportunity and constraint. Its rising strategic weight is evident, but the channels of influence are shifting in ways that challenge traditional approaches. Western engagement – focused on governance, conditional financing, and targeted investment – remains important but largely project-based. China has advanced a systems-oriented model integrating infrastructure, finance, and supply chains, while India leverages entrenched commercial networks and Russia sustains a limited, adaptive security role.

These approaches coexist within a competition. African states actively diversify partnerships, constraining external dominance. The key distinction lies in scale: influence is increasingly determined not by discrete projects, but by the capacity to shape interconnected systems – transport corridors, financial flows, and value chains. As a result, today’s infrastructure, industrial capacity, and financial frameworks will define long-term trade patterns and value capture.

Competition on the Swahili coast is incremental rather than confrontational. Its effects will materialize over time, as supply chains evolve and economic influence recalibrates. Actors able to operate at the systems level will be best positioned to shape these outcomes.

MORE ON THE TOPIC:

excellent work from sf.

china is working very hard to secure its future. any success in africa will be attacked by the currency cartel. in 10 years any globalist attacks become impossible. when increased prosperity is shared it can not be defeated.

amazing work done by south front. it’s very comprehensive and still accessible

informative and well documented.

nice to see an article on sf dealing with the positive ramifications of the brics concept, and no alluding to the deprivations of the inbred death cult chosenite a*seholes.

please move away from all of the west’s systems from banking to the w.ho. to the west’s culture their and fake christianity.

look inwards as much as possible. burkina faso is on the right path. namibia too.

brics is a good partnership too.

africa really is the cradle of humanity. do not invite any european country to invest in africa. look to the chinese & the russians who treat africa and their people as equal partners.